Why We Think the Spring Rally May Extend Into the Summer

“However beautiful the strategy, you should occasionally look at the results.” – Winston Churchill

- The S&P 500 edged 0.6% higher last week for its eighth weekly gain in the last nine weeks.

- Historically, markets have rallied during the summer months of an election year when an incumbent is running.

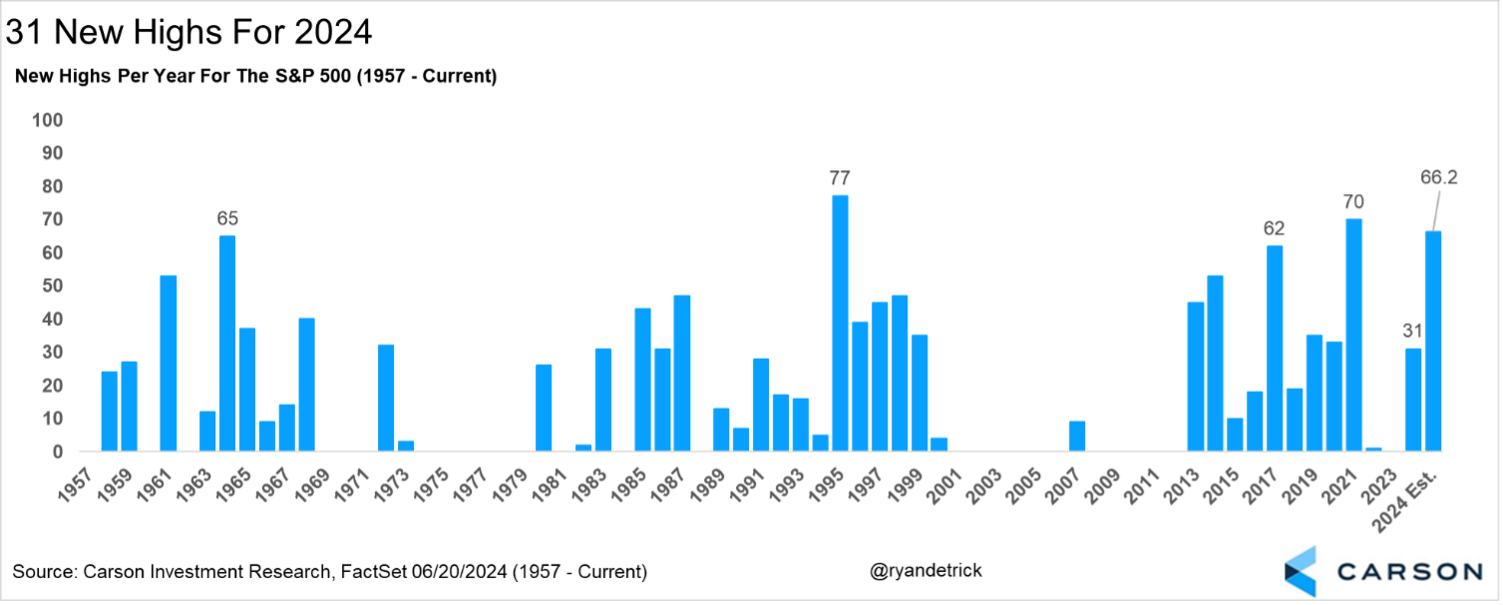

- More than 30 new all-time highs in a year has seen an average gain over the year of nearly 20%. 2024 already has 31 new all-time highs.

- There was much ado about nothing last week as a fake viral story about the end of a non-existent “petrodollar deal” unnecessarily raised concerns about the dollar.

- The dollar continues to play an important role facilitating trade, providing liquidity, and supporting economic stability and it will be difficult to dislodge as the world’s dominant currency.

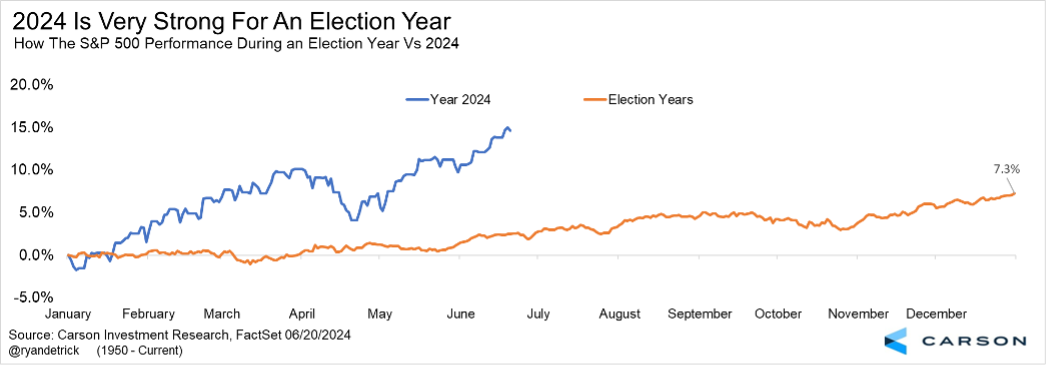

The amazing bull market continues and 2024 is turning into one of the better starts to a year ever. Yes, there have been some much better years, but considering the S&P 500 gained 25% last year, the approximately 15% gain so far this year is really impressive.

One thing that intrigues us is election years usually aren’t that strong early and tend to do better later in the year. In fact, only 1976 among election year was stronger at this point in the year, up 15.6% at the midway point. What happened next? Stocks added another 3% the final six months.

Here’s one way to show how this year isn’t your average election year.

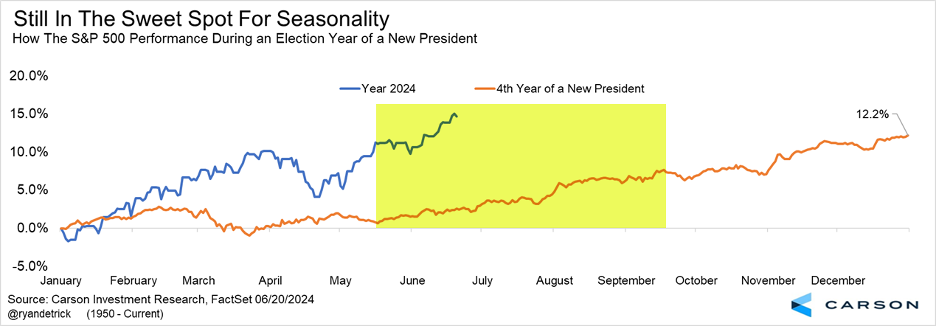

But let’s also be aware that in election years when an incumbent president is running, we are right in the middle of what tends to be a good part of the year. From mid-May to late September stocks do pretty darn well. Yes, we’ve had a heck of a run, but this could be a clue that the summer rally isn’t over yet.

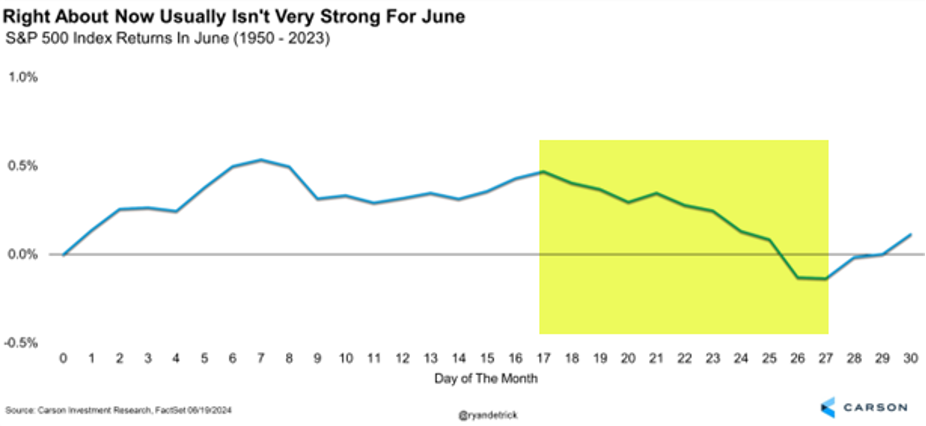

Now let’s be clear, stocks have been on a super strong rally lately. After gaining nearly 5% in May, stocks are up close to 4% in June so far. 1997 was the most recent year that saw gains of more than 4% in both of those usually tepid months, and stocks gained another 10% the rest of the year. But before we assume stocks will gain 4% in June, let’s be aware the month isn’t over yet and historically the latter part of June tends to be weak. After the run stocks have seen lately, some type of well-deserved break at some point before the end of the month would be perfectly normal.

Here’s one way to look at what we’ve seen so far in 2024. After 118 trading days there have been 31 new all-time highs this year, putting 2024 on pace for more than 66 new all-time highs (ATH), which would be one of the most ever. Looking at other years to see at least 30 new ATHs (remember, we’ve already seen 31), the full year was higher every time (20 out of 20) and up 19.6% on average.

No! Saudi Arabia Is Not Ending Any “Petrodollar Pact”

We received a lot of questions about a viral story that Saudi Arabia was going to end its so-called petrodollar pact last week. To get to the heart of it, Saudi Arabia is not going to stop selling oil in US dollars (USD), and they’re not ending any petrodollar pact. In fact, there is no petrodollar pact, secret or otherwise. So, there’s nothing to renew (or not renew). Nor is there any “paradigm shift” shift in global finance.

The rather mundane truth behind this volcano of misinformation is that the US and Saudi Arabia put together a Joint Bilateral Commission on Economic Cooperation in the 1970s to strengthen US-Saudi relations. Oil prices surged in 1973-74 after the Arab oil embargo, sending inflation surging. Following this unpleasant episode, the US wanted to foster closer ties with the Saudis to avert another crisis. The best way to do that was to get the Saudis to invest the proceeds of their oil sales in the US by buying US assets. Note that this was already happening, with the Saudis starting to invest a lot of their oil wealth in the US. The goal was to continue and enhance this trend. The result of the bilateral commission was that the US would give technical assistance to the Saudis across multiple areas – defense, agriculture, labor, science and technology, industrialization – all of which the Saudis would fund using “petrodollars,” petrodollars simply being the dollars received for selling oil.

Crucially, this arrangement was not a formal deal or treaty, just a combination of economic reality and good diplomacy.

The US built closer ties to a country that could prevent another oil shock. It clearly worked for the Saudis too, as they got 2 things:

- Development assistance from the US

- Assets in a currency (USD) that was liquid and freely convertible (so they could move it around as they liked)

Fast forward to the current day, and the irony behind the rumors is that the US and Saudi Arabia are actually on the verge of signing a historic security agreement, pulling the two countries even closer together from a defense perspective. Also, everything related to the global oil trading systems – financing, transportation, insurance, etc. – is all done in USD. That’s unlikely to change anytime soon, as the network effects are just too strong.

Finally, the US is now the largest oil producer in the world, which means the biggest source of “petrodollars” right now is the US.

So What If the Saudis Don’t Sell Oil in USD ¯\_(ツ)_/¯

Back in the 1970s, the Saudis didn’t have a lot of other options when it came to selling oil. However, now it looks like they do. The Saudis could “diversify” and start selling oil to the Chinese in yuan and to the Indians in rupees. But what comes next? Once they receive Chinese yuan or Indian rupees, what do they do with it? Ideally, they’d buy Chinese or Indian assets with it, i.e. government bonds, stocks, and/or real estate. That may work, but only up to a certain point. There are a lot of constraints to “replacing the dollar.”

For one thing, US assets are a lot more attractive from a return perspective, especially relative to Chinese assets. Chinese and Indian assets are also not as liquid as US assets. There’s not even enough “T-bill” equivalents to park cash in, like the Saudis (or even you or I) can do with US Treasuries.

Just as important, their currencies are not “fully convertible” like the US dollar is. The dollar is easy to buy and sell on the foreign exchange market with few restrictions (the Japanese yen, euro, and pound are also fully convertible). China and India, by contrast, have strict capital controls, which is why their currencies are not easily convertible. The best way to think about this is that you can buy Chinese and Indian assets but selling them and moving money out of these countries is not easy. China and India are unlikely to loosen capital controls anytime soon. If that happened, China in particular would likely see a flood of capital moving out of the country into “safer” places (like the US).

More likely is this scenario: If the Saudis receive yuan or rupees for their oil, they’re likely to hand it over to someone else in exchange for USD (assuming they find takers for it, which may be quite hard to do at scale). And we’re back to the same place.

Here’s Why the Dollar Will Likely Remain Dominant

The USD is unlikely to be dethroned from its top status anytime soon (probably not even in our lifetime). Three reasons why.

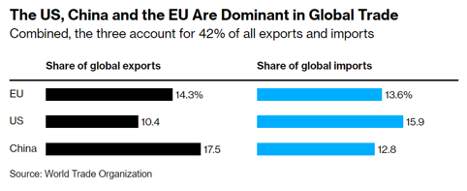

One, global trade is dominated by the US, China, and the EU. But it’s massively skewed, with the US importing much more than it exports. China is the dominant exporter, but even Europe exports more than it imports. All this means the rest of the world is awash in US dollars – which they receive in exchange for supplying Americans with goods. That’s actually a feature of how their economies work, which they rely on in many ways.

And what do they do with the USD they receive? They invest them in the most liquid and deepest capital market in the world, the United States of America.

This dynamic is not going to change unless countries like China start importing a lot more goods from America, which would be very good for American manufacturers and workers. But, for countries like China and Germany to start importing more, their households will have to start earning a larger share of national income. It also means their domestic manufacturers will lose some of their market share. However, the political dynamic in these countries is not going to allow for redistribution from domestic businesses to households.

If you really want to start “worrying” about the dollar’s premier status, a good time would be when the Chinese government implements something like Social Security and Medicare. That’s as good a signal as any that would foreshadow a shift away from the dollar.

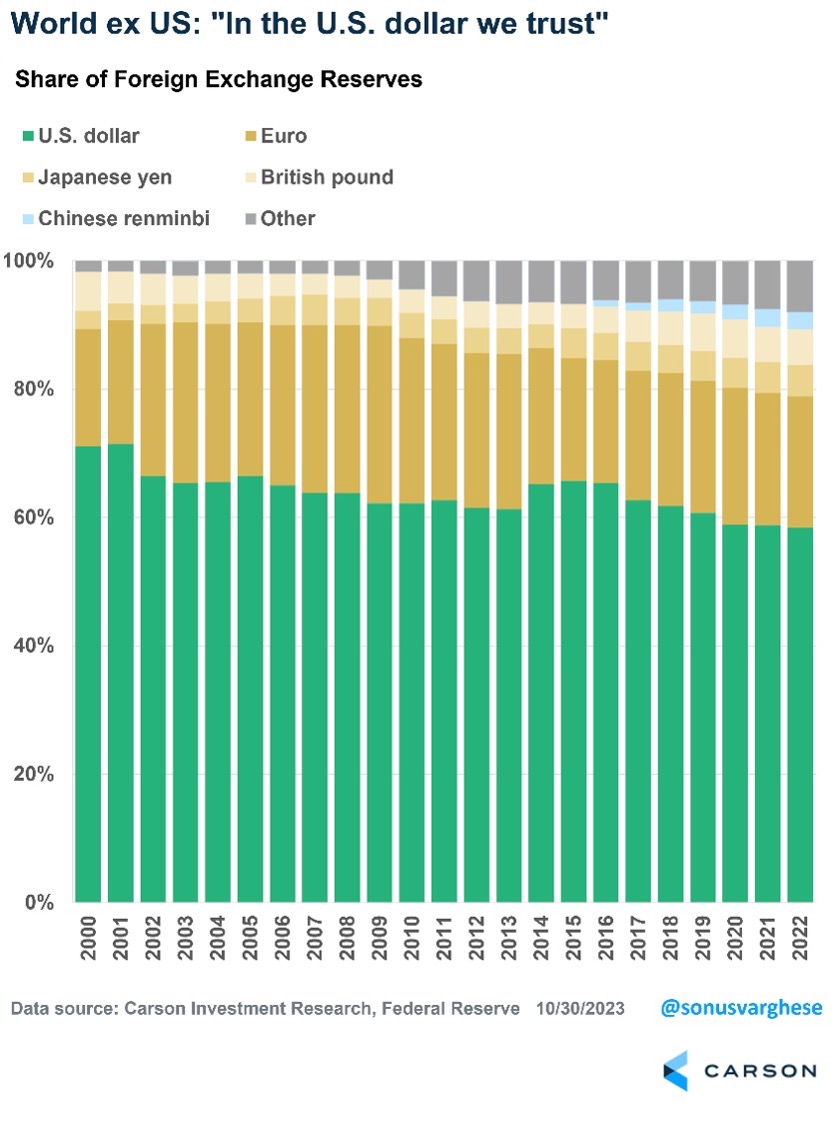

The second reason: The world has confidence in the US, and therefore the dollar. This is because the US has the deepest and most liquid financial markets, thanks to the size and strength of the US economy, open trade and capital flows with few restrictions, strong rule of law, property rights, and a history of enforcement. Despite the US making up 25% of the global economy, about 60% of global foreign currency reserves are in USD. It has fallen from 71% in 2000 but remains far ahead of other currencies as the decline in share has been spread across various currencies.

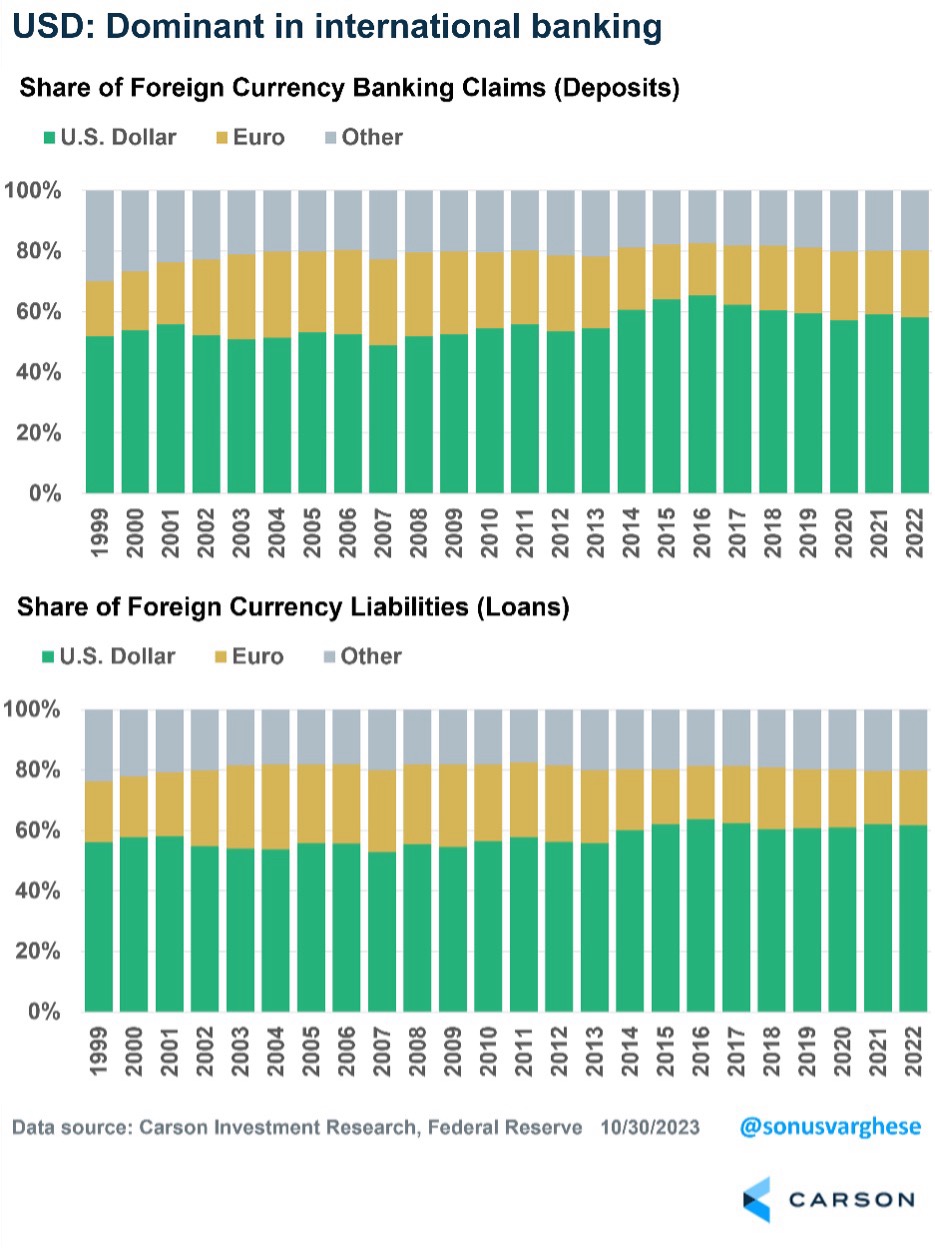

The third reason is that the USD is dominant in trade invoicing and international finance. Outside of Europe, more than 70% of exports are invoiced in US dollars. That’s unlikely to change anytime soon. Again, everyone wants USD because it’s liquid and “safe.” It also means the USD automatically becomes the dominant currency for international banking. Close to 60% of international foreign currency banking claims are in USD, including bank deposits denominated in foreign currency and loans taken out in a foreign currency. That’s been fairly stable since 2000, and actually increased over the past decade.

Foreigners like to borrow in dollars, thanks to its stability. Of the total amount borrowed in foreign currency, USD-based borrowing accounts for 62%, up from 56% in 2012. This is all about network effects and they can be extremely hard to dislodge. It won’t be easy to convince people across the world that they have to move their assets from the USD to another currency, let alone face the risk of actually making the switch.

Could all of these things we laid out above change? Sure, but it’s likely to be a long and very slow process. Our advice: Ignore the viral advertising and trigger seed stories that have come up every few months, really for decades, that some trivial or plain made up news event is going to “crash” the dollar. The global economy is a complex system in which the dollar is deeply embedded. But that’s been an economic strength, as the dollar continues to play an important role facilitating trade, providing liquidity, and supporting economic stability.

This newsletter was written and produced by CWM, LLC. Content in this material is for general information only and not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly. The views stated in this letter are not necessarily the opinion of any other named entity and should not be construed directly or indirectly as an offer to buy or sell any securities mentioned herein. Due to volatility within the markets mentioned, opinions are subject to change without notice. Information is based on sources believed to be reliable; however, their accuracy or completeness cannot be guaranteed. Past performance does not guarantee future results.

S&P 500 – A capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The NASDAQ 100 Index is a stock index of the 100 largest companies by market capitalization traded on NASDAQ Stock Market. The NASDAQ 100 Index includes publicly-traded companies from most sectors in the global economy, the major exception being financial services.

A diversified portfolio does not assure a profit or protect against loss in a declining market.

Compliance Case # 02293069_062424_C